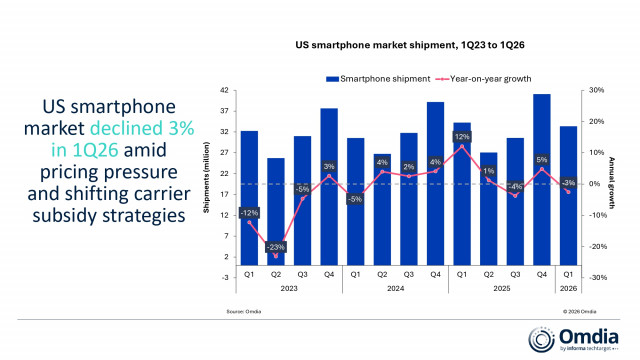

Omdia: US Smartphone Market Declined 3% in 1Q26 Amid Pricing Pressure and Carrier Subsidy Shifts

US smartphone market shipment, 1Q23 to 1Q26

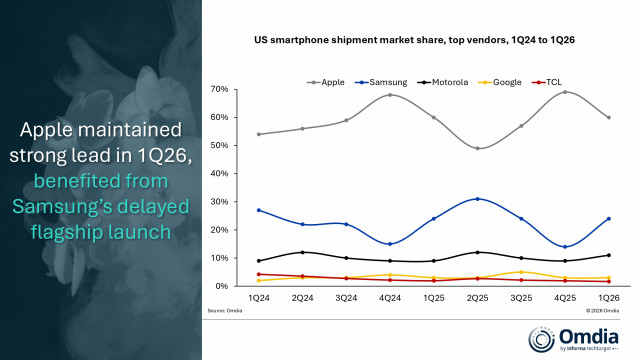

US smartphone shipment market share, top vendors, 1Q24 to 1Q26

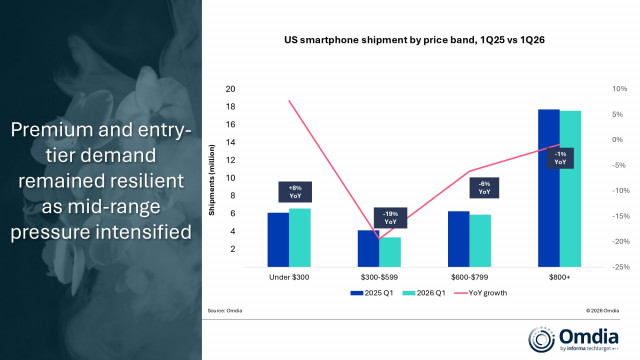

US smartphone shipment by price band, 1Q25 vs 1Q26

· Apple maintained its leading position in Q126 despite a 3% year over year decline. Apple benefited from Samsung’s delayed Galaxy S26 launch, limiting direct premium Android competition. The iPhone 17 series accounted for 70% of Apple’s shipments, while aggressive iPhone 15 prepaid promotions continued supporting demand in lower price tiers.

· Samsung ranked second in Q126, with shipments declining 5% year over year as the delayed Galaxy S26 launch. Despite the later timing, the S26 series showed strong early traction, with pre-orders up nearly 25% versus the S25 series. Samsung relied heavily on prepaid-driven A-series demand during Q1, led by the Galaxy A17.

· Motorola was the only major vendor to grow in Q126, with shipments rising 18% year over year. Growth was driven primarily by the refreshed Moto G portfolio, which accounted for more than 70% of Motorola’s quarterly shipments. Carrier and prepaid channels also appeared to pull forward inventory ahead of Motorola’s April price increases.

· Google shipments fell 7% year over year in Q126, as the Pixel 10 series failed to replicate the momentum of the Pixel 9 lineup a year earlier. The earlier launch of the Pixel 10a helped offset some of the decline, while aggressive carrier promotions remained central to Google’s strategy to expand Pixel demand beyond its core premium user base.

“The US smartphone market is becoming increasingly polarized, with premium and entry-tier devices proving far more resilient,” added Chen. “In 1Q26, the $800+ premium segment declined only 1% year over year, supported by Apple and carrier financing. The sub-$300 segment grew by 8%, helped by prepaid demand, plan-linked promotions, and channel pull-forward ahead of price increases on select value models. Meanwhile, pressure was concentrated in the middle of the market, with the $300-599 segment declining 19% and the $600-799 segment falling 6%. This suggests that rising device costs and more selective carrier subsidies put the most pressure on Android mid-range and mid-to-high-end devices, while premium models and budget devices remained better supported by US channel structures.”

“The US smartphone market is entering a phase where carriers are playing a larger role in moderating how rising device costs reach consumers,” added Chen. “While OEM manufacturer’s suggested retail prices (MSRPs) started moving higher in 1Q 26, most consumers have yet to fully feel the impact because carriers continue to manage affordability through financing, promotions and plan-led offers. However, how long carriers can absorb or delay these increases remains a key question for upgrade demand through the rest of 2026.”

These pressures are expected to continue through the rest of 2026, with Omdia forecasting US smartphone shipments to decline 4% year over year for the full year. Beyond near-term pricing and volume pressure, AI-native devices are emerging as a longer-term strategic watchpoint. While such devices are unlikely to drive immediate smartphone substitution, developments from OpenAI and reported interest from Amazon suggest AI-driven interfaces could gradually reshape how consumers perceive smartphone upgrade value.

(To view the table, please visit https://www.businesswire.com/news/home/20260527603016/en/)

ABOUT OMDIA

Omdia, part of TechTarget, Inc. d/b/a Informa TechTarget (Nasdaq: TTGT), is a technology research and advisory group. Our deep knowledge of tech markets grounded in real conversations with industry leaders and hundreds of thousands of data points, make our market intelligence our clients’ strategic advantage. From R&D to ROI, we identify the greatest opportunities and move the industry forward.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260527603016/en/

Website: https://omdia.tech.informa.com/

Contact

Omdia

Fasiha Khan

fasiha.khan@omdia.com

Eric Thoo

eric.thoo@omdia.com

기자 발굴부터 성과 측정까지 PR 업무 시간을 절반으로

-

7월 15일 17:50